How a Personal Pension Works

As there are no restrictions on the number of personal pensions you can belong to, they can provide additional retirement benefits to run alongside your workplace pension scheme. When choosing a personal pension, we always advise clients to carefully consider the flexibility of pension package, so that your contributions can remain the same regardless of whether you change jobs or stop working.

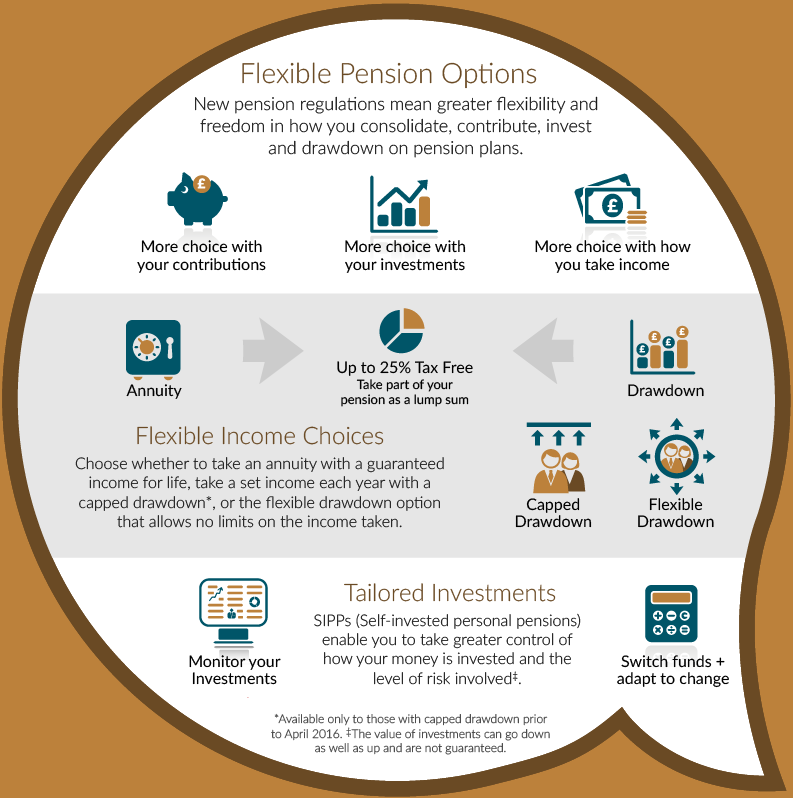

There are a wide range of choices out there and it is often difficult to clearly understand which pension will best suit your requirements. Again the watch word is “flexibility”. All contributions you make are invested and there is a huge choice of investment funds. We offer advice that puts in clear terms the risk profile of funds when weighed against the anticipated levels of return.

Risk Strategy

While a higher risk strategy can yield a higher return, it’s important to remember that funds go down as well as up, and in many cases clients prefer a lower risk strategy that provides smaller returns but more security for their hard-earned money. Talk to us today about how we can help you find the right pension strategy.